Understanding Citizenship Status for FHA Loans

Navigating FHA mortgage guidelines just got more complicated—especially for borrowers who aren’t U.S. citizens. To understand how the recent rule change affects you or your clients, let’s first clarify how FHA loans categorize citizenship status:

U.S. Citizens

These borrowers hold U.S. citizenship by birth or naturalization and remain fully eligible for FHA loans.

Permanent Residents (Green Card Holders)

These individuals are legally allowed to live and work in the U.S. permanently. FHA still considers them eligible, as long as they can provide documentation from U.S. Citizenship and Immigration Services (USCIS) verifying their status.

✅ Example: Maria is a green card holder working as a nurse in Maryland. She remains eligible for an FHA loan, provided she submits her USCIS documentation.

Non-Permanent Residents

This category includes individuals with temporary visas (e.g., H1B, F1), asylum seekers, and undocumented immigrants. These borrowers will no longer be eligible for FHA-insured loans after May 25, 2025.

❌ Example: Ali, on a work visa, received an FHA preapproval in March 2025. If his case number is assigned after May 25, 2025, he will not qualify under the new rule.

FHA Rule Change Overview: Mortgagee Letters TI-490 & ML 2025-09

On March 26, 2025, HUD released Mortgagee Letters TI-490 and ML 2025-09, officially updating FHA loan eligibility guidelines.

Key Highlights of the Rule Change

- Non-permanent residents are no longer eligible for FHA-insured loans.

- This rule applies to all FHA case numbers assigned on or after May 25, 2025.

- It affects both Title I (property improvement/manufactured housing) and Title II (standard FHA loans and HECMs) programs.

- Borrowers must be U.S. citizens or lawful permanent residents—including those from Micronesia, the Marshall Islands, or Palau—to qualify.

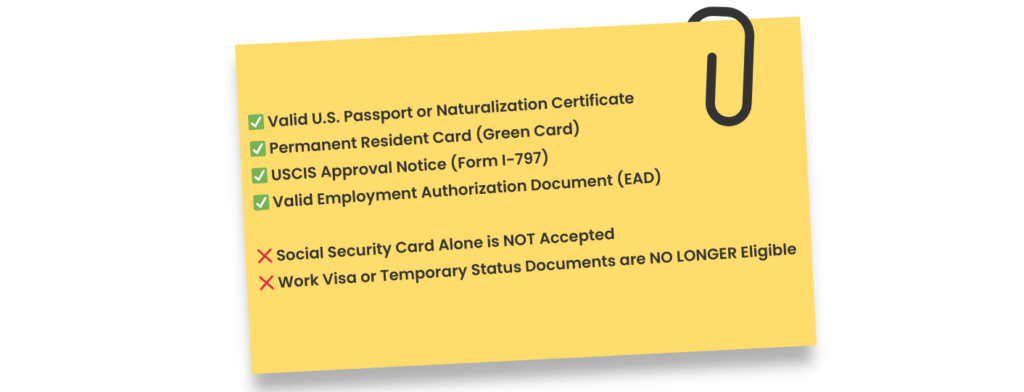

What Documentation Is Now Required?

The revised mortgage guidelines now enforce stricter documentation requirements to confirm eligibility:

- A Social Security card alone is no longer enough.

- Permanent residents must present valid USCIS documentation (e.g., I-551 or I-797 form).

- Citizenship verification may require a naturalization certificate or U.S. passport.

This shift aligns with recent executive orders focused on ensuring federal benefits, including FHA loans, are only extended to lawful residents.

What This Means for Borrowers and Lenders

Borrowers with FHA Preapprovals

If you’re a non-permanent resident with an FHA preapproval, your ability to close depends on your case number assignment date. After May 25, 2025, you’ll need to transition to a conventional loan or alternative financing.

Industry-Wide Policy Alignment

Federal Hill Mortgage: Your Partner in Navigating FHA Changes

This rule change may feel overwhelming, but you’re not alone. At Federal Hill Mortgage, we specialize in helping clients adjust to shifting mortgage guidelines. Here’s how we can help:

Converting FHA Preapprovals to Conventional

Our team excels in analyzing FHA preapprovals and determining viable paths toward conventional financing, often with comparable rates and terms.

Personalized Guidance in Real Time

We work one-on-one with borrowers and real estate agents, offering clear advice and efficient solutions customized to your unique situation.

Deep Industry Knowledge

With decades of experience, our mortgage professionals have successfully navigated countless regulatory changes—and we’re prepared to do it again for you.

Why Act Now?

Waiting until your FHA case number is assigned may limit your options. If you or your client is a non-permanent resident, the time to act is before May 25, 2025.

- Don’t lose your dream home over eligibility issues.

- Don’t let a stalled loan derail your closing timeline.

Need Help Navigating the New FHA Loan Rules?

Need Help Navigating the New FHA Loan Rules?

If you’re a non-permanent resident affected by the new FHA eligibility rules, don’t wait until it’s too late. Our expert team at Federal Hill Mortgage can help you transition your FHA preapproval to a conventional loan and explore alternative financing solutions. Real estate agents — we’re here to support your clients through every regulatory change with clarity and speed.

Let’s make sure your financing strategy stays on track.

Start My Application