An extra $36,600 can show up in different ways depending on your situation and your local market.

1) You May Have More “Acceptable Homes,” Not Just More Homes

A lot of buyers aren’t trying to maximize purchase price. They’re trying to avoid regret.

That extra buying power can mean moving from:

- “Only homes that need major work” → “Move-in ready options that cost slightly more”

- “One neighborhood that barely fits the budget” → “A wider radius with better inventory”

When you ask “how much house can I afford in 2026?”, the answer isn’t just a price—it’s access to better options and more breathing room in your monthly payment.

2) Negotiation Leverage Is Back

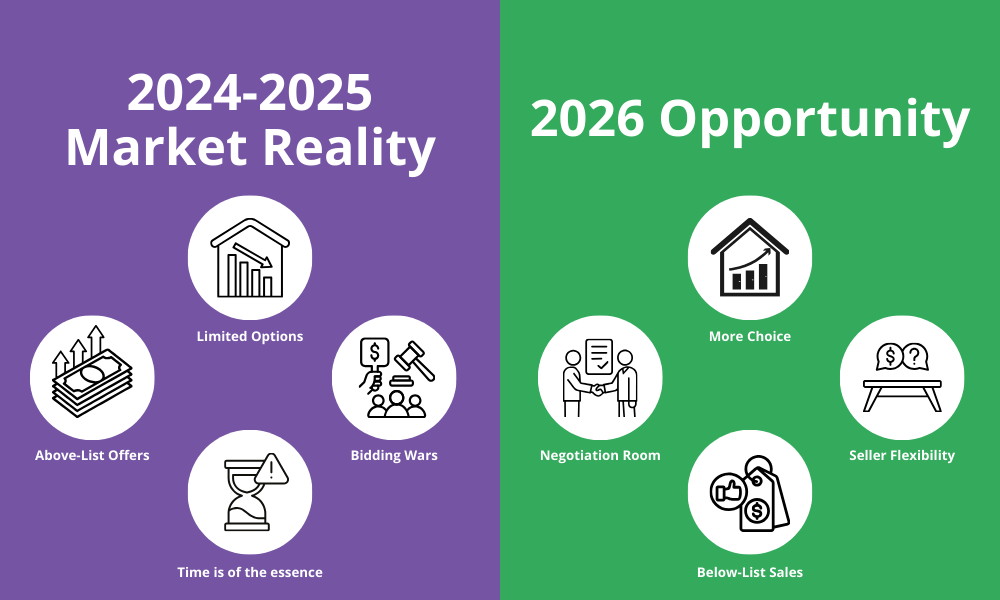

Even with affordability improving, buyers aren’t rushing like they did during the frenzy.

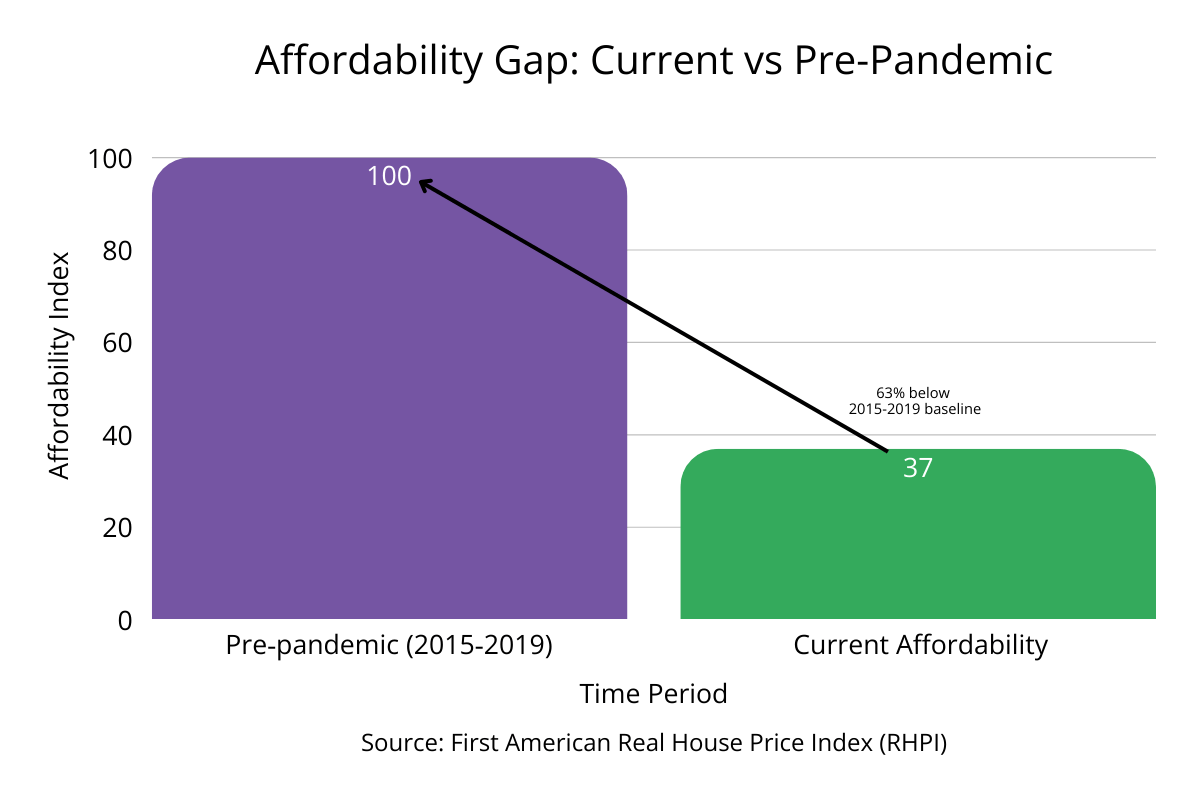

Redfin data shows:

- Homes took a median 63 days to go under contract

- Only 19.2% sold above list

- Average sale-to-list ratio: 97.7%

That combination signals a more normal market where sellers have to compete. It’s why smart buyers are now focusing on negotiation leverage and terms, not just trying to win a price war.

3) Concessions Can Matter More Than a Lower Price

In a buyer-friendlier market, sellers often consider:

- Repair credits (if inspection reveals issues)

- Closing cost assistance (reduces cash needed at closing)

- Rate buydowns (lowers your monthly payment in early years)

- Flexibility on timing and contingencies (gives you breathing room)

The key: ask for concessions that improve your financial outcome. A well-targeted $10K credit for repairs might reduce your monthly payment more than shaving $20K off the purchase price. Learn more about closing cost assistance options available to you.

4) Build an Offer Strategy Instead of Guessing

When markets are tight, buyers often have one move: go higher.

When markets slow down, you can build a strategy around:

- Which homes are overpriced and likely to negotiate

- Which sellers are motivated by timeline (and will trade price for certainty)

- Which concessions actually help you close smoothly

This is where working with a lender who can run scenarios quickly helps. You can respond with confidence instead of emotion.